import numpy as np

import pandas as pd

from matplotlib.pyplot import subplots

from statsmodels.datasets import get_rdataset

import sklearn.model_selection as skm

from ISLP import load_data , confusion_table

from ISLP.models import ModelSpec as MS1. imports

from sklearn.tree import (DecisionTreeClassifier as DTC ,

DecisionTreeRegressor as DTR, plot_tree, export_text)

from sklearn.metrics import (accuracy_score, log_loss)

from sklearn.ensemble import (RandomForestRegressor as RF, GradientBoostingRegressor as GBR)

from ISLP.bart import BART2. Data

Carseats = load_data('Carseats')

High = np.where(Carseats.Sales > 8, "Yes", "No")3. 단순 나무 모형 적용

model = MS(Carseats.columns.drop('Sales'), intercept=False)

D = model.fit_transform(Carseats)

feature_names = list(D.columns)

X = np.asarray(D)

clf = DTC(criterion='entropy', max_depth=3, random_state=0)

# 깊이는 3으로, 손실함수는 엔트로피 이용

clf.fit(X, High)DecisionTreeClassifier(criterion='entropy', max_depth=3, random_state=0)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

DecisionTreeClassifier(criterion='entropy', max_depth=3, random_state=0)

- 분류 문제에서 예측오차, 손실함수의 값, 의사결정 나무 확인

accuracy_score(High , clf.predict(X))0.79- Residual deviance: $ -2 m k n{mk} {mk} $

resid_dev = np.sum(log_loss(High , clf.predict_proba(X)))

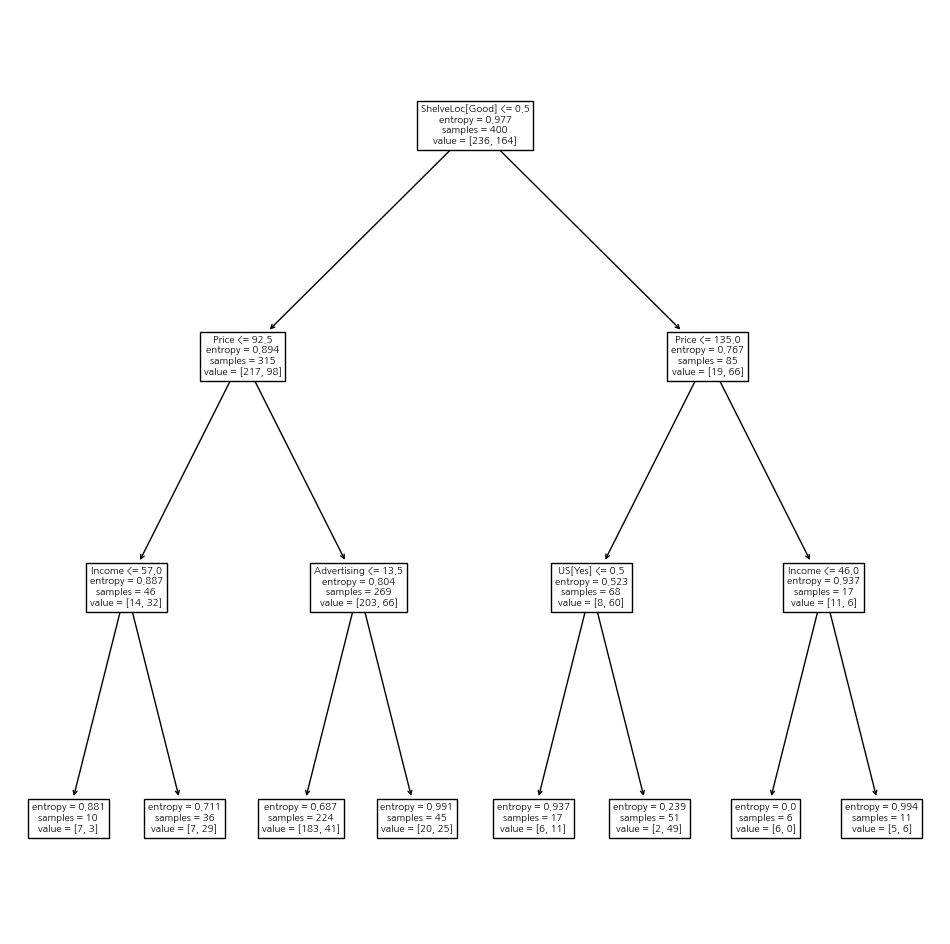

resid_dev0.4710647062649358ax = subplots(figsize=(12,12))[1]

plot_tree(clf, feature_names=feature_names, ax=ax);

print(export_text(clf, feature_names=feature_names, show_weights=True))

# weights: 0과 1의 비중|--- ShelveLoc[Good] <= 0.50

| |--- Price <= 92.50

| | |--- Income <= 57.00

| | | |--- weights: [7.00, 3.00] class: No

| | |--- Income > 57.00

| | | |--- weights: [7.00, 29.00] class: Yes

| |--- Price > 92.50

| | |--- Advertising <= 13.50

| | | |--- weights: [183.00, 41.00] class: No

| | |--- Advertising > 13.50

| | | |--- weights: [20.00, 25.00] class: Yes

|--- ShelveLoc[Good] > 0.50

| |--- Price <= 135.00

| | |--- US[Yes] <= 0.50

| | | |--- weights: [6.00, 11.00] class: Yes

| | |--- US[Yes] > 0.50

| | | |--- weights: [2.00, 49.00] class: Yes

| |--- Price > 135.00

| | |--- Income <= 46.00

| | | |--- weights: [6.00, 0.00] class: No

| | |--- Income > 46.00

| | | |--- weights: [5.00, 6.00] class: Yes

- Validation error 확인

validation = skm.ShuffleSplit(n_splits=1, test_size=200, random_state=0)

results = skm.cross_validate(clf, D, High, cv=validation)

results['test_score']array([0.685])- 두 개의 데이터셋으로 쪼개서 훈련과 평가 진행

(X_train, X_test, High_train, High_test) = skm.train_test_split(X, High, test_size=0.5, random_state=0)

clf = DTC(criterion='entropy', random_state=0)

clf.fit(X_train, High_train)

accuracy_score(High_test, clf.predict(X_test))0.735- 훈련 데이터에서 CV로 최적의 pruning 을 선택

ccp_path = clf.cost_complexity_pruning_path(X_train, High_train)

kfold = skm.KFold(10, random_state=1, shuffle=True)

grid = skm.GridSearchCV(clf, {'ccp_alpha': ccp_path.ccp_alphas}, refit=True,cv=kfold,

scoring='accuracy')

grid.fit(X_train, High_train)

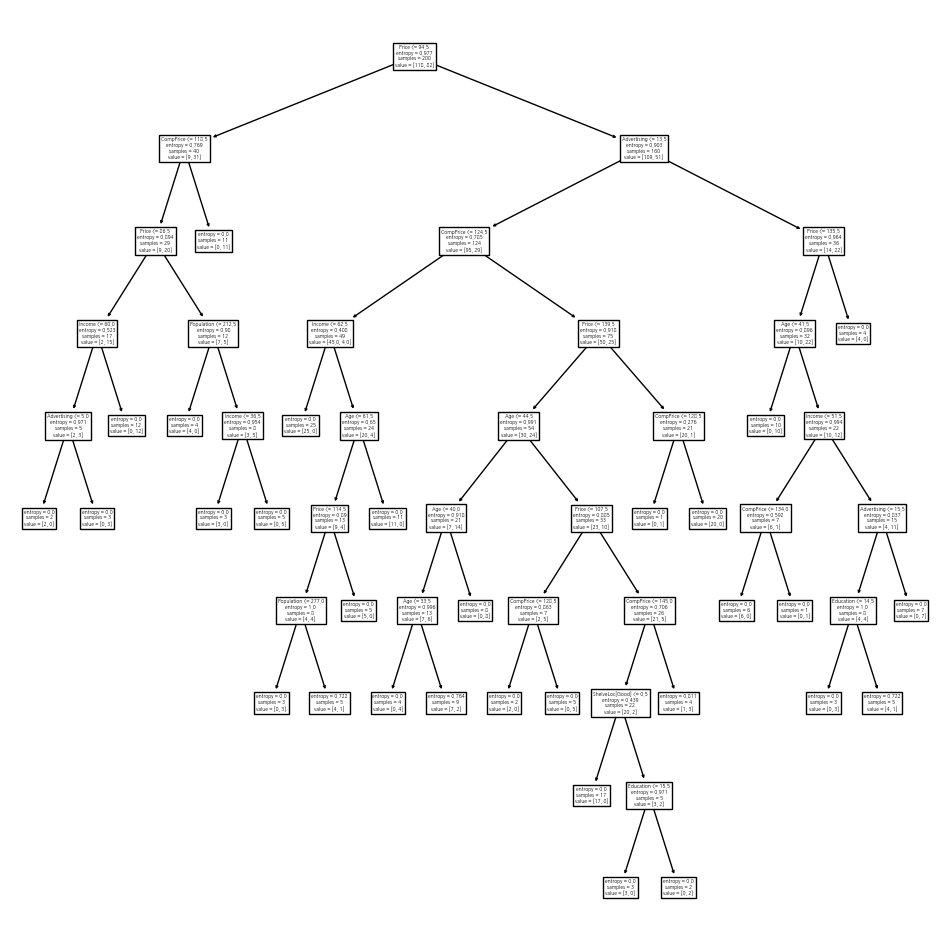

grid.best_score_0.685- CV로 선택된 최적의 의사결정나무를 그림

ax = subplots(figsize=(12, 12))[1]

best_ = grid.best_estimator_

plot_tree(best_, feature_names=feature_names, ax=ax);

best_.tree_.n_leaves30

- 훈련 데이터에서 모형을 구축하고 평가 데이터에서 혼동행렬을 봄

print(accuracy_score(High_test, best_.predict(X_test)))

confusion = confusion_table(best_.predict(X_test), High_test)

print(confusion)0.72

Truth No Yes

Predicted

No 94 32

Yes 24 50- 보스턴 데이터 로딩 및 의사결정나무(회귀분석) 분석 진행

Boston = load_data("Boston")

model = MS(Boston.columns.drop('medv'), intercept=False)

D = model.fit_transform(Boston)

feature_names = list(D.columns)

X = np.asarray(D)(X_train, X_test, y_train, y_test) = skm.train_test_split(X, Boston['medv'],test_size=0.3, random_state=0)

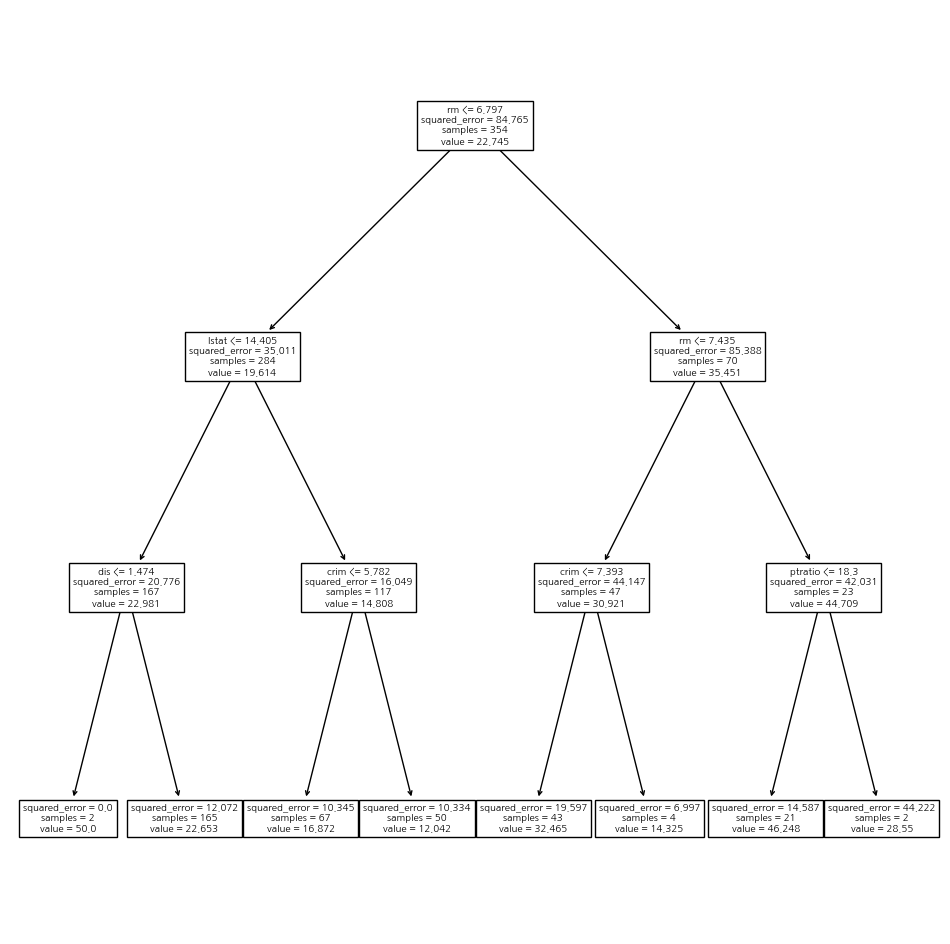

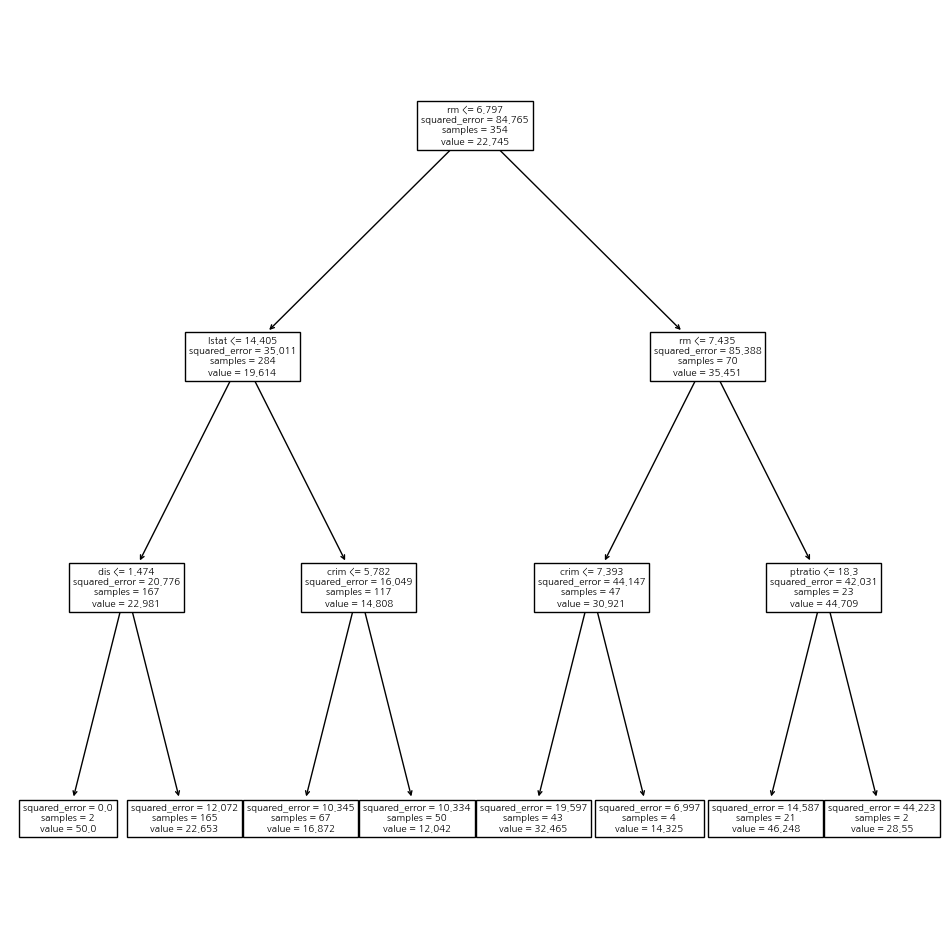

reg = DTR(max_depth=3)

reg.fit(X_train , y_train)

ax = subplots(figsize=(12,12))[1]

plot_tree(reg, feature_names=feature_names, ax=ax);

- CV를 통한 최적의 pruning을 진행

ccp_path = reg.cost_complexity_pruning_path(X_train , y_train)

kfold = skm.KFold(5, shuffle=True, random_state =10)

grid = skm.GridSearchCV(reg, {'ccp_alpha': ccp_path.ccp_alphas}, refit=True, cv=kfold,

scoring='neg_mean_squared_error')

G = grid.fit(X_train, y_train)

best_ = grid.best_estimator_

np.mean((y_test - best_.predict(X_test))**2)28.06985754975404ax = subplots(figsize=(12,12))[1]

plot_tree(G.best_estimator_, feature_names=feature_names, ax=ax);

4. RF(Random Forests)

- 보스턴 데이터에 대한 랜덤 포레스트 진행

bag_boston = RF(max_features=X_train.shape[1], random_state=0)

bag_boston.fit(X_train , y_train)RandomForestRegressor(max_features=12, random_state=0)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

RandomForestRegressor(max_features=12, random_state=0)

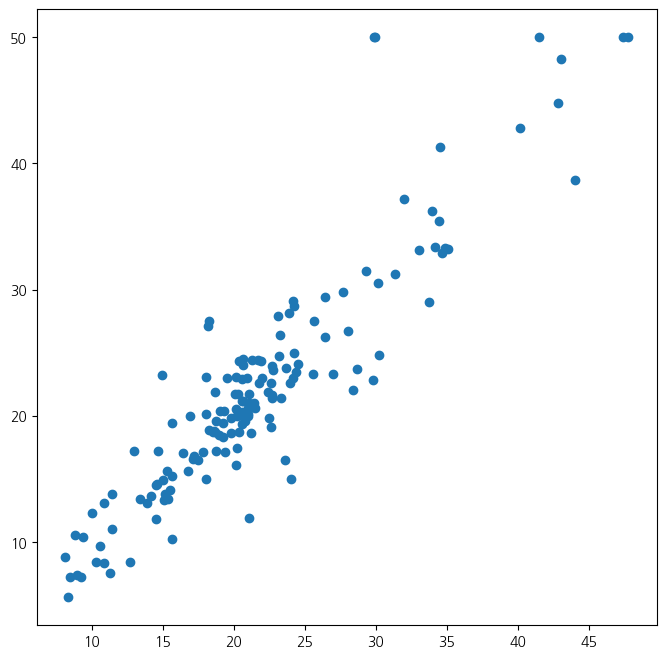

- 예측값과 산점도를 통해서 정확도를 확인, 예측오차를 계산

ax = subplots(figsize=(8,8))[1]

y_hat_bag = bag_boston.predict(X_test)

ax.scatter(y_hat_bag , y_test)

np.mean((y_test - y_hat_bag)**2)14.634700151315787

- 랜덤 포레스트에서 사용하는 변수의 개수를 조정

bag_boston = RF(max_features=X_train.shape[1],

n_estimators=500, random_state=0).fit(X_train , y_train)

y_hat_bag = bag_boston.predict(X_test)

print(np.mean((y_test - y_hat_bag)**2))

# usinbg sqrt(p) variables

RF_boston = RF(max_features=6, random_state=0).fit(X_train , y_train)

y_hat_RF = RF_boston.predict(X_test)

print(np.mean((y_test - y_hat_RF)**2))14.605662565263161

20.04276446710527- 변수의 중요도를 의미하는 importance를 확인

feature_imp = pd.DataFrame( {'importance':RF_boston.feature_importances_}, index=feature_names)

print(feature_imp.sort_values(by='importance', ascending=False)) importance

lstat 0.356203

rm 0.332163

ptratio 0.067270

crim 0.055404

indus 0.053851

dis 0.041582

nox 0.035225

tax 0.025355

age 0.021506

rad 0.004784

chas 0.004203

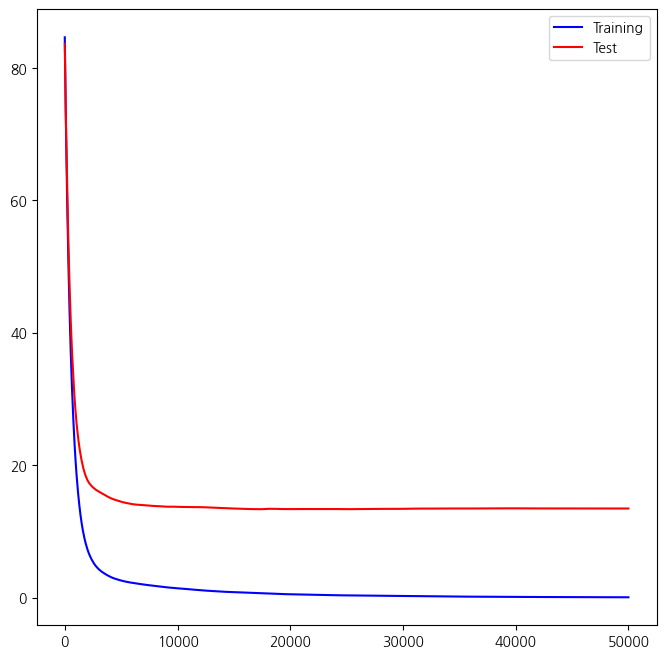

zn 0.002454- 그래디언트 부스팅을 진행

- 동원된 의사결정나무는 5000개, 최대 깊이는 3, 학습률은 0.001

boost_boston = GBR(n_estimators=50000, learning_rate =0.001, max_depth=3,

random_state=0)

boost_boston.fit(X_train , y_train)

test_error = np.zeros_like(boost_boston.train_score_)

for idx , y_ in enumerate(boost_boston.staged_predict(X_test)):

test_error[idx] = np.mean((y_test - y_)**2)

plot_idx = np.arange(boost_boston.train_score_.shape[0])

ax = subplots(figsize=(8,8))[1]

ax.plot(plot_idx, boost_boston.train_score_, 'b', label='Training')

ax.plot(plot_idx, test_error, 'r', label='Test')

ax.legend();

- 위 그림에서 단계 진행에 따른 훈련과 평가 예측오차를 확인, 아래는 예측오차 계산

y_hat_boost = boost_boston.predict(X_test)

np.mean((y_test - y_hat_boost)**2)13.461677803903655- 학습률 조정에 따른 예측오차

boost_boston = GBR(n_estimators=5000, learning_rate=0.2, max_depth=3,random_state=0)

boost_boston.fit(X_train, y_train)

y_hat_boost = boost_boston.predict(X_test);

np.mean((y_test - y_hat_boost)**2)14.5015145537195655. 베이지안 의사결정나무

- 평가 데이터에서 예측오차 확인

bart_boston = BART(random_state=0, burnin=5, ndraw=15)

# burn-in: 앞의 몇 개를 잘라냄, ndraw: 몇 개의 연쇄 샘플링을 할지 경정

bart_boston.fit(X_train , y_train)

yhat_test = bart_boston.predict(X_test.astype(np.float32))

np.mean((y_test - yhat_test)**2)22.145009458109225- 변수의 중요도

var_inclusion = pd.Series(bart_boston.variable_inclusion_.mean(0), index=D.columns)

print(var_inclusion)crim 26.933333

zn 27.866667

indus 26.466667

chas 22.466667

nox 26.600000

rm 29.800000

age 22.733333

dis 26.466667

rad 23.666667

tax 24.133333

ptratio 24.266667

lstat 31.000000

dtype: float64